Sales :423-900-8928

Service / Parts :423-900-8929

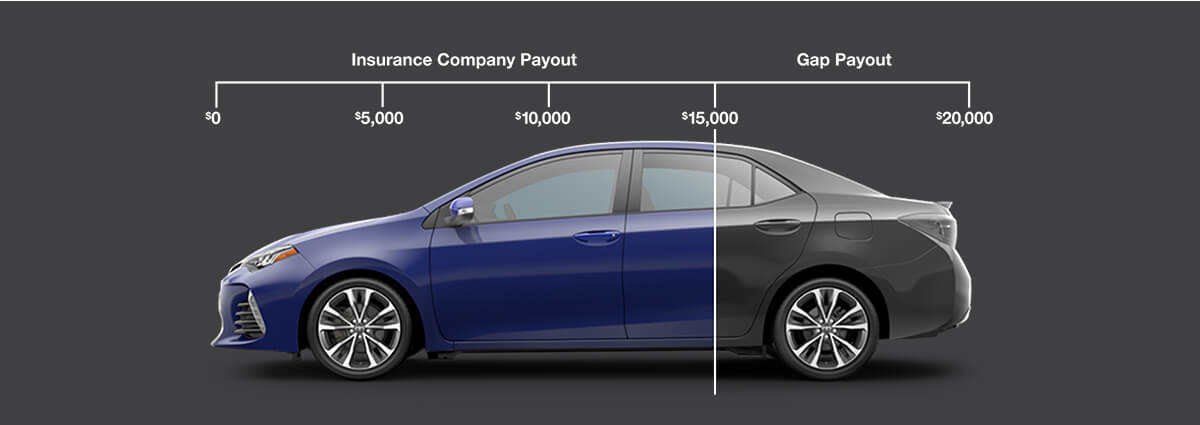

GAP Coverage

When buying a vehicle, especially a new one, it's not rare for a driver to owe more than the vehicle is actually worth, because of depreciation and other causes. Thanks to this, if your vehicle is stolen or totaled, the payout from your insurance company may not be enough to cover the entire amount you currently owe.

If you happen to get into one of these situations, you'll be glad to have Guaranteed Auto Protection (GAP) insurance. This special coverage bridges the gap between what you receive from your insurance and how much you find yourself still owing. What makes this coverage even more valuable, though, is the fact that it gets rolled into your auto loan, slightly raising each monthly payment. You'll be covered and barely realize the difference in your bill.

When To Consider GAP Insurance

If you’re interested in learning more about GAP coverage or you have any additional questions, contact us today, or stop by our dealership at 3124 Bristol HWY Johnson City, TN 37601. We look forward to serving our customers from Johnson City, TN, and throughout Bristol and Kingsport!

Call Us

Call Us Directions

Directions